Explainer: What a U.S. debt ceiling extension means for bond markets

An image illustration reveals U.S. 100 greenback financial institution notes taken in Tokyo August 2, 2011. REUTERS/Yuriko Nakao

NEW YORK, Oct 12 (Reuters) – Gridlock over the U.S. debt ceiling could have been quickly resolved, however a longer-term answer has additionally been deferred. Final week’s truce appeased the bond market a bit, however traders are nonetheless eyeing default dangers forward of a brand new December deadline.

WHAT IS THE DEBT CEILING NOW?

After weeks of wrangling, the , the utmost quantity the U.S. authorities can borrow as directed by Congress to fulfill its monetary obligations, by $480 billion to what’s now $28.9 trillion. It now goes to the U.S. Home of Representatives for a vote on Tuesday earlier than President Joe Biden can signal it into legislation. That is anticipated to cowl debt financing wants by means of no less than early December.

That may give Congress extra time to cross a longer-term debt ceiling extension by means of reconciliation, analysts mentioned. BofA Securities, in a analysis observe, mentioned it believes U.S. Treasury funding may transcend December and into January and even February.

WHAT DOES THE U.S. TREASURY NEED TO PAY OUT OF THE DEBT LIMIT INCREASE?

The U.S. Treasury is anticipated to spend about two-thirds of the $480 billion of latest borrowing authority pretty quickly. Cash market analysis agency Wrightson Capital, in a analysis observe, mentioned the Treasury, by legislation, should reinstate belief fund balances that had been disinvested throughout a “debt issuance suspension interval” (DISP). The Treasury’s newest weekly debt ceiling exercise report final Friday confirmed authorities belief funds had been owed $301 billion in non-marketable securities as of Oct. 6. Wrightson mentioned changing these belief fund securities will depart the Treasury with lower than $200 billion of conventional borrowing authority when the debt ceiling enhance formally takes impact later this week.

WOULD THE TREASURY STILL BE ABLE TO TAP INTO EXTRAORDINARY MEASURES IF THE $480 BILLION RUNS OUT?

Estimates from Wrightson confirmed the Treasury is probably going to make use of up the rest of its common borrowing by the primary week of November. If that’s the case, Treasury Secretary Janet Yellen could should declare a brand new DISP, which might enable the division to faucet into its extraordinary measures once more. That provides the Treasury roughly $300 billion of accounting flexibility, which needs to be sufficient to cowl probably all of its borrowing wants, for the rest of the yr, Wrightson mentioned.

WILL TREASURY BILL SUPPLY INCREASE WITH THE RISE IN DEBT LIMIT?

BofA Securities initiatives there may very well be a greater than a $300 billion near-term enhance in invoice provide after the short-term debt restrict is signed into legislation. This estimate is predicated on Treasury’s present and goal money balances. The payments will probably take the type of one-month and short-dated money administration payments.

WHAT ARE THE NEAR-TERM MARKET IMPLICATIONS OF THE DEBT LIMIT EXTENSION?

Because of the extension, the danger of a short-term debt default has eased, if not deferred to December. The thinly traded one-year credit score default swaps that might repay in case of a U.S. authorities default traded at 14.9 foundation factors final Friday, after spiking to twenty-eight foundation factors earlier than the debt restrict enhance.

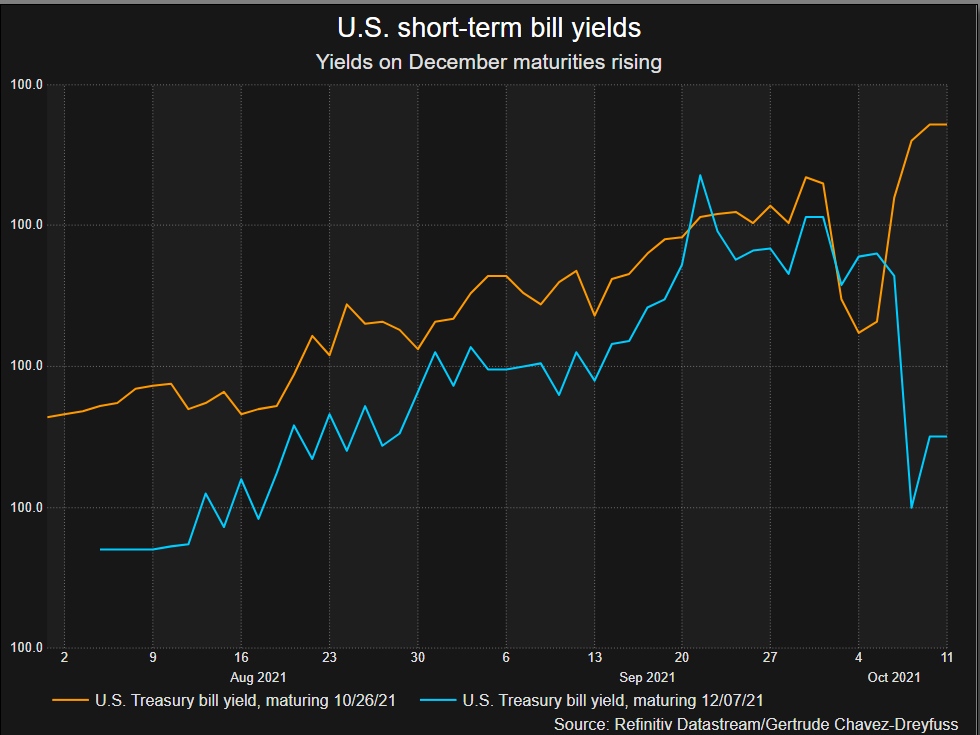

Yields on U.S. payments, with late October maturities, have additionally fallen. For example, the yield on the Oct. 26 maturity fell to 4 foundation factors final Friday, from as excessive as practically 20 foundation factors final week. The stress, nonetheless, has shifted to the early December maturities, the place yields have doubled. The yield on the December 7 maturity rose to eight foundation factors final Friday, from 4 foundation factors per week earlier.

Outdoors of the invoice market, nonetheless, there are few indicators of stress. Within the U.S. repurchase (repo) market, traders are maintaining a detailed eye on the Treasury invoice collateral pledged to them in each in a single day and time period trades. Barclays, in a analysis observe, wrote that whereas lenders are watching debt ceiling-sensitive CUSIPs, or identification numbers, they haven’t excluded them from the eligibility listing. That implies some expectation of a debt ceiling decision.

Reporting by Gertrude Chavez-Dreyfuss; Enhancing by Megan Davies and Paul Simao

: