Banks beware, Amazon and Walmart are cracking the code for finance

LONDON, Sept 17 (Reuters) – Anybody generally is a banker nowadays, you simply want the appropriate code.

World manufacturers from Mercedes and Amazon to IKEA and Walmart are chopping out the standard monetary intermediary and plugging in software program from tech startups to supply clients the whole lot from banking and credit score to insurance coverage.

For established monetary establishments, the warning indicators are flashing.

So-called embedded finance – a elaborate time period for firms integrating software program to supply monetary companies – means Amazon can let clients “purchase now pay later” once they take a look at and Mercedes drivers can get their automobiles to pay for his or her gas.

To make certain, banks are nonetheless behind many of the transactions however buyers and analysts say the chance for conventional lenders is that they may get pushed additional away from the entrance finish of the finance chain.

And meaning they will be additional away from the mountains of information others are hoovering up concerning the preferences and behaviours of their clients – information that might be essential in giving them an edge over banks in monetary companies.

“Embedded monetary companies takes the cross-sell idea to new heights. It is predicated on a deep software-based ongoing information relationship with the patron and enterprise,” mentioned Matt Harris, a companion at investor Bain Capital Ventures.

“That’s the reason this revolution is so essential,” he mentioned. “It signifies that all the great danger goes to go to those embedded firms that know a lot about their clients and what’s left over will go to banks and insurance coverage firms.”

WHERE DO YOU WANT TO PLAY?

For now, many areas of embedded finance are barely denting the dominance of banks and despite the fact that some upstarts have licences to supply regulated companies similar to lending, they lack the size and deep funding swimming pools of the largest banks.

But when monetary know-how corporations, or fintechs, can match their success in grabbing a bit of digital funds from banks – and boosting their valuations within the course of – lenders might have to reply, analysts say.

Stripe, for instance, the funds platform behind many websites with purchasers together with Amazon and Alphabet’s Google, was in March.

Accenture estimated in 2019 that new entrants to the funds market had amassed 8% of revenues globally – and that share has risen over the previous yr because the pandemic boosted digital funds and hit conventional funds, Alan McIntyre, senior banking trade director at Accenture, mentioned.

Now the main focus is popping to lending, in addition to full off-the-shelf digital lenders with a wide range of merchandise companies can decide and select to embed of their processes.

“The overwhelming majority of client centric firms will be capable to launch monetary merchandise that may permit them to considerably enhance their buyer expertise,” mentioned Luca Bocchio, companion at enterprise capital agency Accel.

“That’s the reason we really feel enthusiastic about this area.”

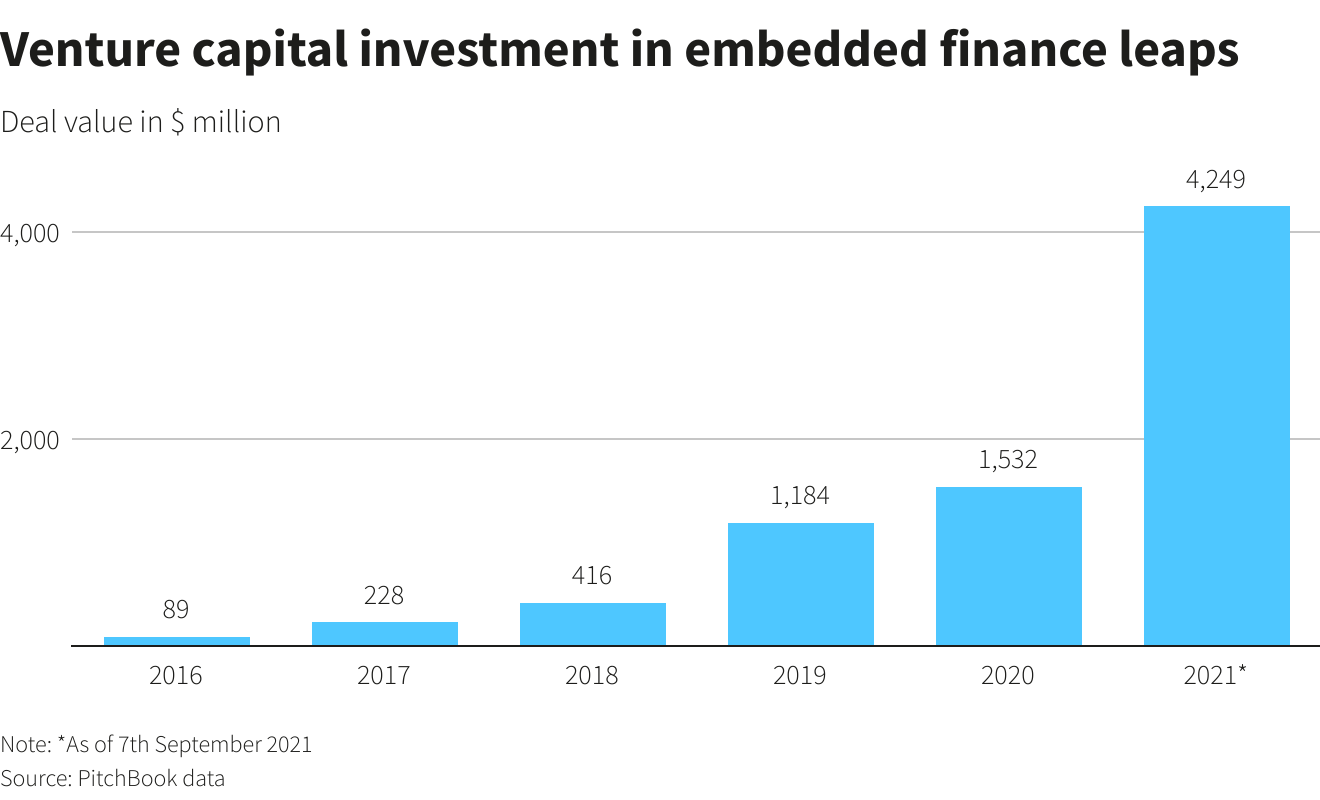

Up to now this yr, buyers have poured $4.25 billion into embedded finance startups, nearly thrice the quantity in 2020, information supplied to Reuters by PitchBook exhibits.

Main the best way is Swedish purchase now pay later (BNPL) agency Klarna which raised $1.9 billion.

DriveWealth, which sells know-how permitting firms to supply fractional share buying and selling, attracted $459 million whereas buyers put $229 million into Solarisbank, a licensed German digital financial institution which gives an array of banking companies software program.

Shares in Affirm , in the meantime, surged final month when it teamed up with Amazon to supply BNPL merchandise whereas rival U.S. fintech Sq. mentioned final month it was shopping for Australian BNPL agency Afterpay for $29 billion.

Sq. is now price $113 billion, greater than Europe’s most beneficial financial institution, HSBC , on $105 billion.

“Massive banks and insurers will lose out if they do not act rapidly and work out the place to play on this market,” mentioned Simon Torrance, founding father of Embedded Finance & Tremendous App Methods.

YOU NEED A LOAN!

A number of different retailers have introduced plans this yr to increase in monetary companies.

Walmart launched a fintech startup with funding agency Ribbit Capital in January to develop monetary merchandise for its workers and clients whereas IKEA took a minority stake in BNPL agency Jifiti final month.

Automakers similar to Volkswagen’s Audi and Tata’s Jaguar Land Rover have experimented with embedding cost know-how of their autos to take the effort out of paying, in addition to Daimler’s Mercedes.

“Clients count on companies, together with monetary companies, to be instantly built-in on the level of consumption, and to be handy, digital, and instantly accessible,” mentioned Roland Folz, chief government of Solarisbank which offers banking companies to greater than 50 firms together with Samsung.

It is not simply finish customers being focused by embedded finance startups. Companies themselves are being tapped on the shoulder as their digital information is crunched by fintechs similar to Canada’s Shopify .

It offers software program for retailers and its Shopify Capital division additionally gives money advances, primarily based on an evaluation of greater than 70 million information factors throughout its platform.

“No service provider involves us and says, I would really like a mortgage. We go to retailers and say, we predict it is time for funding for you,” mentioned Kaz Nejatian, vice chairman, product, service provider companies at Shopify.

“We do not ask for enterprise plans, we do not ask for tax statements, we do not ask for revenue statements, and we do not ask for private ensures. Not as a result of we’re benevolent however as a result of we predict these are unhealthy alerts into the chances of success on the web,” he mentioned.

A Shopify spokesperson mentioned funding goes from $200 to $2 million. It has supplied $2.3 billion in cumulative capital advances and is valued at $184 billion, nicely above Royal Financial institution of Canada , the nation’s greatest conventional lender.

CONNECTED FUTURE?

Shopify’s lending enterprise is, nonetheless, nonetheless dwarfed by the large banks. JPMorgan Chase & Co , for instance, had a client and group mortgage ebook price $435 billion on the finish of June.

Main advances into finance by firms from different sectors is also restricted by regulators.

Officers from the Financial institution for Worldwide Settlements, a consortium of central banks and monetary regulators, warned watchdogs final month to familiarize yourself with the rising affect of know-how corporations in finance.

Bain’s Harris mentioned monetary regulators had been taking the method that as a result of they do not know methods to regulate tech corporations they’re insisting there is a financial institution behind each transaction – however that didn’t imply banks would stop fintechs encroaching.

“They’re proper that the banks will all the time have a job but it surely’s not a really remunerative function and it includes little or no possession of the client,” he mentioned.

Forrester analyst Jacob Morgan mentioned banks needed to resolve the place they wish to be within the finance chain.

“Can they afford to struggle for buyer primacy, or do they really see a extra worthwhile path to market to grow to be the rails that different individuals run on high of?” he mentioned. “Some banks will select to do each.”

And a few are already preventing again.

Citigroup has teamed up with Google on financial institution accounts, Goldman Sachs is offering bank cards for Apple and JPMorgan is shopping for 75% of Volkswagen’s funds enterprise and plans to increase to different industries. 06:00:00

“Connectivity between completely different techniques is the long run,” mentioned Shahrokh Moinian, head of wholesale funds, EMEA, at JPMorgan. “We wish to be the chief.”

Reporting by Anna Irrera and Iain Withers; Enhancing by Rachel Armstrong and David Clarke

: