Analysis: Chinese property debt issuers face ‘Evergrande premium’ as worries mount

A employee walks inside the development web site of a undertaking developed by China Evergrande Group in Beijing, China September 22, 2021. REUTERS/Carlos Garcia Rawlins

HONG KONG, Sept 23 (Reuters) – As uncertainty looms over cash-strapped China Evergrande Group , seizing up China’s junk bond market, strain is constructing on its friends to entry contemporary funding to repay notes price almost $300 billion due over the following two years.

As soon as its top-selling developer, Evergrande now looms as one in every of China’s largest-ever restructurings as a crackdown on debt ends a freewheeling period of constructing with borrowed cash which grew to become notorious for ghost cities and roads to nowhere.

Evergrande will default on a greenback bond if it fails to pay curiosity due on Thursday inside 30 days, and the chance is {that a} messy liquidation drags down the entire property sector, which accounts for 1 / 4 of the nation’s gross home product.L1N2QP048

The nervousness has resulted in a handful of Chinese language actual property builders having their rankings downgraded by companies as concern swirls about their debt and compensation talents, which, in flip, will weigh on their borrowing prices.

Debt bankers stated few corporations had been all for tapping the marketplace for contemporary borrowings in the intervening time, as Evergrande’s destiny remained unclear, and that any who should method the market would in all probability need to pay up.

“Debt is being re-priced and a few builders could also be shut out,” Michel Lowy, CEO of asset administration group SC Lowy, advised Reuters. “Not your complete sector,” he stated, however “buyers will definitely be extra cautious about which builders to finance.”

International buyers have been on tenterhooks as debt fee obligations of Evergrande, labouring beneath a $305 billion mountain of debt, triggered fears its malaise may pose systemic dangers to China’s monetary system.

Chinese language property developer bonds often yield between 4% and 12%, if not greater, relying on their credit score rankings and energy of their stability sheet and up to date modest offers have been on the higher finish of that vary.

Redsun Properties Group Ltd , for instance, which raised $210 million in Might at a coupon of seven.3% , issued a $200 million bond on Monday at a coupon of 9.5% .

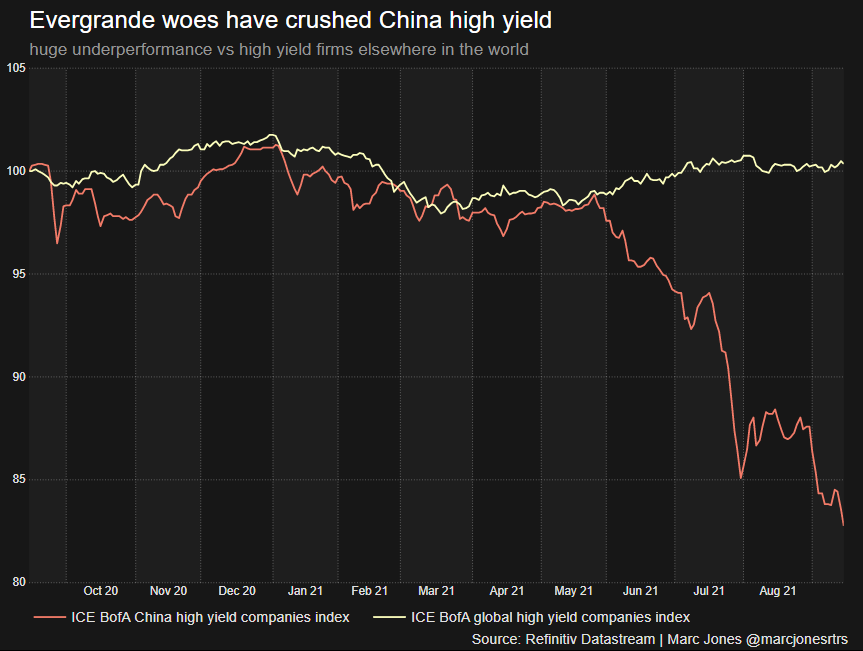

An index of high-yield Chinese language debt has been tanking for months – whilst world credit have rallied – as issues at Evergrande’s predicament have seeped throughout the market.

An estimated $32 billion price of bonds issued by Chinese language builders are on account of be refinanced by the top of 2021, based on Dealogic information, earlier than main transactions expire in 2022.

Almost $125 billion price of developer debt – led by Evergrande which has 5 of the highest ten greatest maturations price almost $6.3 billion – is due subsequent 12 months, the Dealogic figures confirmed. An additional $140.7 billion will mature in 2023.

The figures embody each onshore and offshore bonds issued in {dollars} and yuan by Chinese language builders.

“If we had been to see a deal this week, the foremost response can be ‘nicely, there must be a premium’,” stated a Hong Kong-based debt banker who couldn’t be named as he was not authorised to talk to the media.

“Nobody has paid an Evergrande premium but up to now few weeks however will they be paying that premium by the top of the 12 months? We have to see how lengthy this lasts.”

MONEY WILL FIND A WAY

China’s markets reopened on Wednesday after holidays however had been quiet within the lead up to what’s often a busy interval in October when companies have finalised their quarterly stability sheets and have a tendency to look to faucet markets.

Some Chinese language property builders have begun asset gross sales and began in search of alternate funding sources, in a single case shareholders, as widening spreads add to regulatory difficulties in accessing capital.

Guangzhou R&F Properties Co , which based on Fitch has $1.9 billion in debt maturing inside 12 months, has already turned elsewhere – elevating as a lot as $2.5 billion by promoting a subsidiary and taking loans from its greatest shareholders.

Others are struggling, with shares in Sinic Holdings (Group) cratering virtually 90% earlier than being suspended from commerce on Monday, after a Fitch outlook downgrade that has since been adopted by a rankings minimize to CCC+ by S&P on Tuesday.

Sinic has failed to speak a transparent compensation plan, S&P International Scores stated.

Redsun and R&F declined to touch upon Thursday and Sinic didn’t instantly reply to a request for remark.

“I do not suppose the door of the capital markets will shut utterly for Chinese language property builders, however it is going to be a matter of when and who’s trying to increase cash or refinance debt,” Jonathan Leitch, Hogan Lovells companion, advised Reuters.

“There may be a small premium hooked up for some issuers, however there may be a lot liquidity in world markets presently that cash will discover its approach to these corporations.”

Reporting by Scott Murdoch in Hong Kong and Tom Westbrook in Singapore. Further reporting by Clare Jim; Modifying by Sumeet Chatterjee and Nick Macfie

: