U.S. mortgage rates surge to 6-month high -MBA

New townhomes are seen in a subdivision with different close by properties which might be beneath development in Tampa, Florida, U.S., Could 5, 2021. REUTERS/Octavio Jones

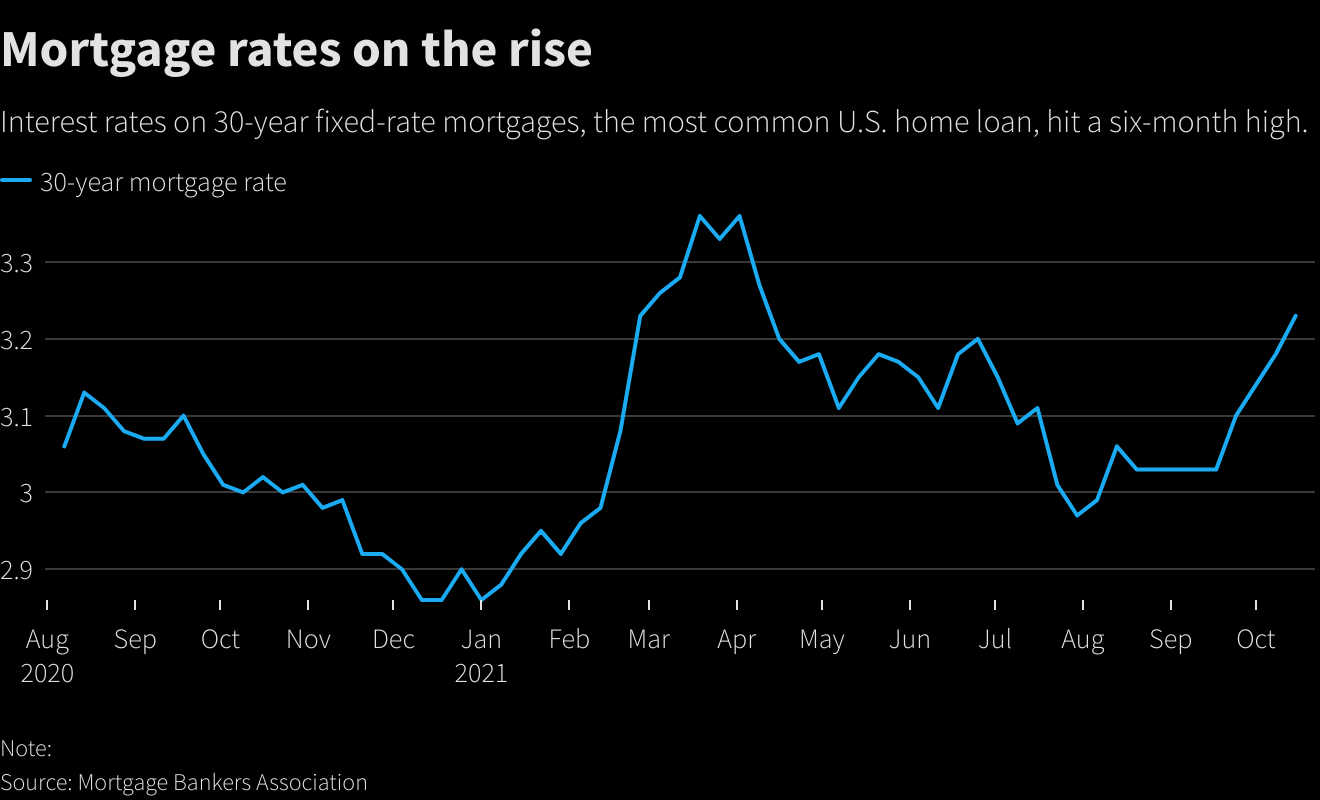

Oct 20 (Reuters) – Rates of interest on the most well-liked kind of U.S. dwelling mortgage shot to a six-month excessive final week as international charges continued their march greater in opposition to a bout of stiff inflation and expectations that central banks will again additional away from their pandemic-era easy-money insurance policies.

The contract charge on a 30-year fastened charge mortgage climbed to three.23% within the week ended Oct. 15 from 3.18% the week earlier than, the Mortgage Bankers Affiliation reported on Wednesday in its weekly survey of situations within the U.S. dwelling lending market. That was the very best stage since early April and is up by greater than 1 / 4 proportion level for the reason that finish of July.

The rise in charges helped drive general mortgage-application volumes down by 6.3% to the bottom since July, led by a 7.1% drop in refinancing functions, the MBA stated. Refinancing utility volumes are additionally at their lowest since July, simply fractionally above their lowest ranges since early 2020.

Purposes for loans to purchase a house fell 4.9% to the bottom since early September.

“Buy exercise declined and was 12% decrease than a 12 months in the past,” stated Joel Kan, MBA’s Affiliate Vice President of Financial and Trade Forecasting. “Inadequate housing provide and elevated home-price progress proceed to restrict choices for would-be patrons.”

How shortly that state of affairs is resolved stays the large unknown within the U.S. residential actual property market. On Tuesday, the Commerce Division reported that U.S. homebuilding unexpectedly fell in September and residential development permits dropped to a one-year low amid acute shortages of uncooked supplies and labor.

In the meantime, international rates of interest proceed to grind upward as central banks just like the U.S. Federal Reserve sign the times of crisis-era lodging are nearing their finish within the face of inflation charges operating at their highest in a long time because of provide bottlenecks and labor shortages.

The Fed is broadly anticipated at its subsequent assembly in two weeks to announce plans to begin scaling again its purchases of $120 billion a month of U.S. Treasuries and mortgage-backed securities as a primary step towards a normalization of coverage.

The yield on the 10-year U.S. Treasury word , essentially the most influential benchmark safety in figuring out mortgage rates of interest, hit its highest since Could on Wednesday and has climbed almost half a proportion level since late July.

Reporting by Dan Burns; Modifying by Andrea Ricci

: